How much money should you borrow for college? You might have heard the rule of thumb that you shouldn't borrow more than what you'll make in your first year out of college, but there's more to consider than just a straight-dollar amount.

The real answer is that your total debt should be proportional to your earning potential. That means it's important to consider things like your choice of school, your major, and much of your future take-home pay will have to go toward loan repayment.

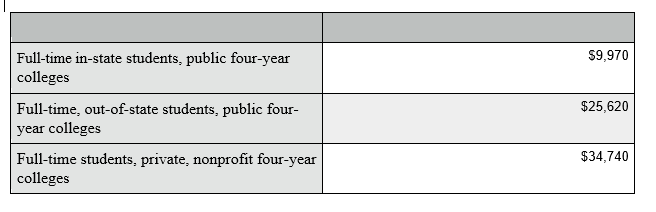

1. Where will you go to school?

Are you going to a four-year private university or to a state school? As you can see, the price of college varies significantly depending on what you choose:

Source: The College Board’s Trends in College Pricing report.

That's not to say a private school can't be affordable — many of them offer excellent financial aid packages, and you can always use scholarships and grants to fill the gap. But generally speaking, you can save a lot of money by going to a state school or a community college, which would also save you room and board costs because you can live at home.

You can compare the price of your choice schools by using our College Cost Calculator.

2. How much will you make after graduation?

While you probably don't need to base your entire decision on how much you expect to make post-graduation, the rule of thumb that we mentioned above 9you shouldn't borrow more than what you'll make in your first year of employment) should still be one of the many factors to consider.

Think of it this way: Would you be willing to borrow $50,000 for an education? Well, it depends on your earning potential. If you're an electrical engineering major, you may be more willing and able to borrow more than the average student. That's because the average starting salary for electrical engineering grads is $62,428, according to Forbes, compared to a starting salary of just $35,626 for those who earn a degree in Pre-K and kindergarten education.

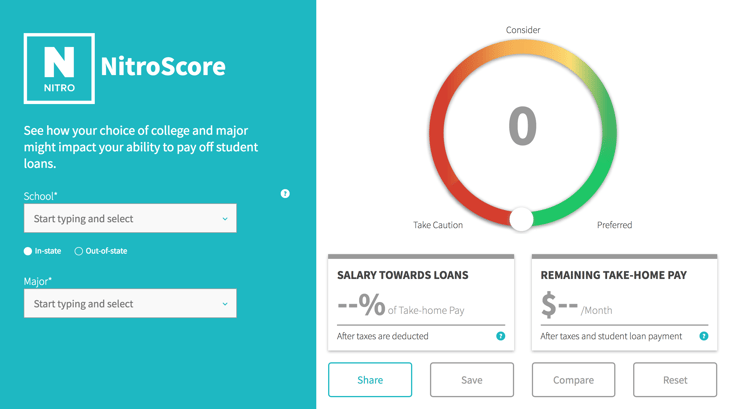

NitroScore can help you figure out how your choice of school and degree impact your ability to repay your debt.

Thinking about this before you take the plunge is a practical way of going about your education, and it can help you avoid the mistake of borrowing too much for a career that doesn't pay well. In the end, you're responsible for your debt regardless of how much you earn.

3. How much of your take-home will have to go toward student loans?

After graduation, you usually have a six-month grace period before you have to start paying your student loans. That doesn't leave you much time to prepare for repayment. So you need to consider how much you can afford to pay each month on your potential salary.

Use NitroScore to compare the possibilities:

The NitroScore tool allows you to figure out how much of your potential salary will go toward your student loan payment depending on your degree and school. It also gives you an affordability score so you know where you stand.

It's not all about loans

Remember that borrowing money isn't the only way to pay for school. Grants, scholarships, and work-study can go a long way to funding your education. Read more about financial aid on our blog.