There’s a certain thrill to going to a big state university. Besides the massive name recognition, there are often huge sports programs to participate in or root for, a buffet of majors to choose from, and a vibrant on-campus life.

But what happens after you toss your mortar board in the air and enter the so-called real world? Is going to a big state school a good investment when it comes to your future?

That’s a question we explored in a landmark research study on Student Debt and Future Earnings. We looked at over 4,600 colleges and universities in the U.S. to find out which schools offered the best value, and which schools might cause you to take on more debt than you anticipated.

The truth about big state schools

Public colleges and universities are often less expensive for one simple reason: they receive funding from the state.

Because these institutions are usually non-profit, that means that more of your tuition dollars are going toward your education, rather than toward efforts that may boost the bottom line.

If that sounds like a good deal, it often is. Investing more money into education may translate to having a wider course selection, more professors, and better facilities.

The return on your investment

In our study, we determined the value of over 4,600 colleges and universities by looking at two criteria:

- The typical amount of debt carried by graduates

- Graduates’ expected earnings 10 years after graduation

Surveying for these two numbers allowed us calculate the debt-to-earnings ratio for various schools.

This ratio is extremely important because it paints a more comprehensive picture of what life could look like after graduation.

Think about it: high earnings are obviously a desirable goal. But high earnings combined with crippling debt is a very different outcome.

A favorable debt-to-earnings ratio may mean the difference between living a comfortable (or even lavish) lifestyle vs. living paycheck to paycheck.

It’s probably no surprise that our research showed the most-favorable outcomes at private, non-profit institutions. That category includes schools such as Harvard, Stanford, and Princeton.

However, beyond this “elite” tier of schools, we found many schools, including a substantial amount of large public universities, that provided a highly favorable return on a tuition investment.

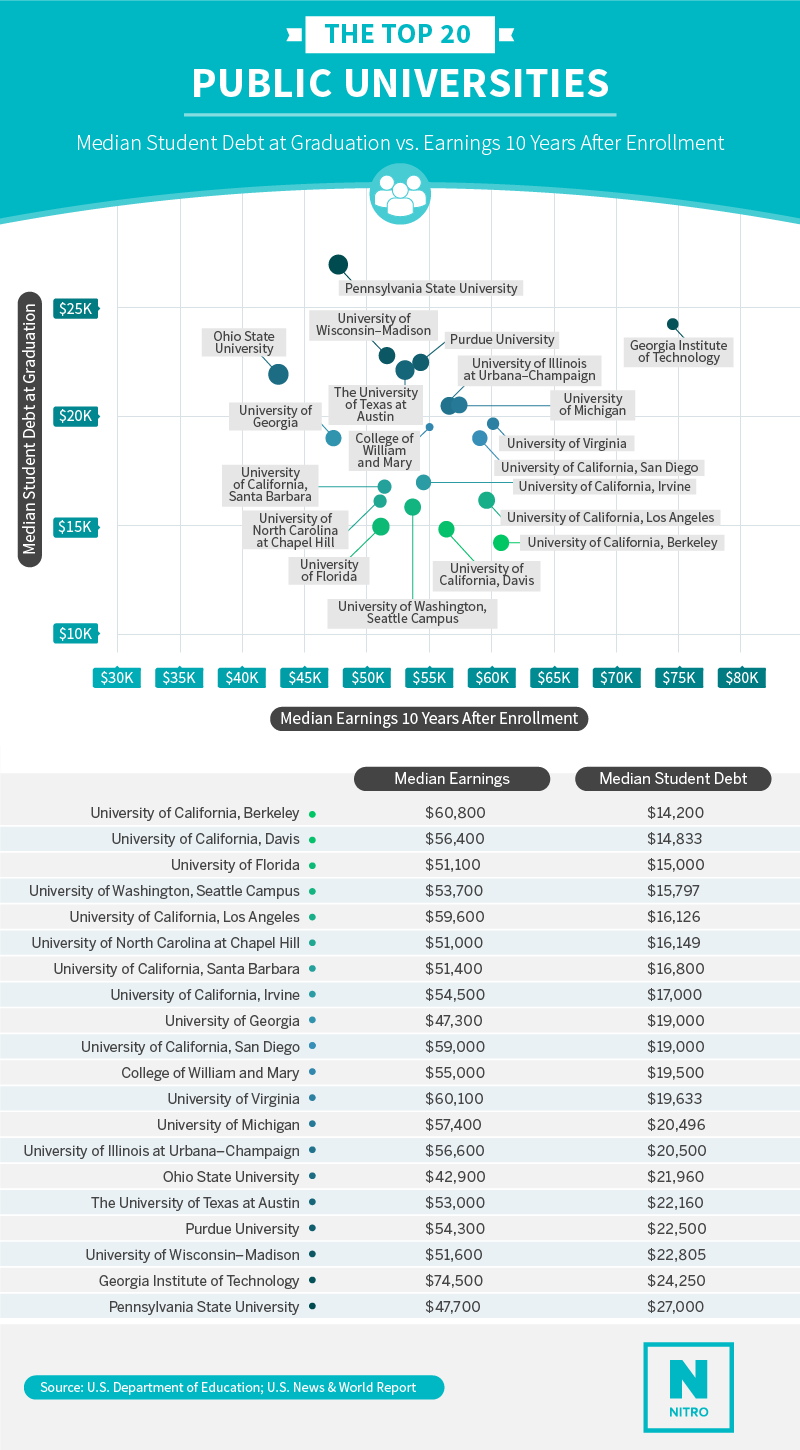

Our research showed that students who attended the top 20 best-valued public universities typically reported incomes ranging from $42,900-$74,500 ten years after graduation and carried student loan debt from $14,200-$27,000.

Here are the top 20 public universities according to our research.

Want to find out more about which schools provide the best value for your tuition dollar?

Check out our special report on Student Debt and Future Earnings to learn more.