The Ultimate Guide to Student Loan Forgiveness

Show of hands: Who hasn’t typed “student loan forgiveness” into a search engine? It’s the dream we all share.

Here, we’re going to talk about whether that dream can become a reality for you or not. The truth is, student loan forgiveness is possible. The reality check is that it’s not a straight-forward process.

Only in certain situations, you can have your federal student loan forgiven, canceled, or discharged.

In this article, we’ll cover the following topics:

What is student loan forgiveness?

Under certain programs, your outstanding student loan balance can be forgiven, meaning that it’s discharged or cancelled.

These are some of the most common types of loan forgiveness programs:

Public Service Loan Forgiveness (PSLF)

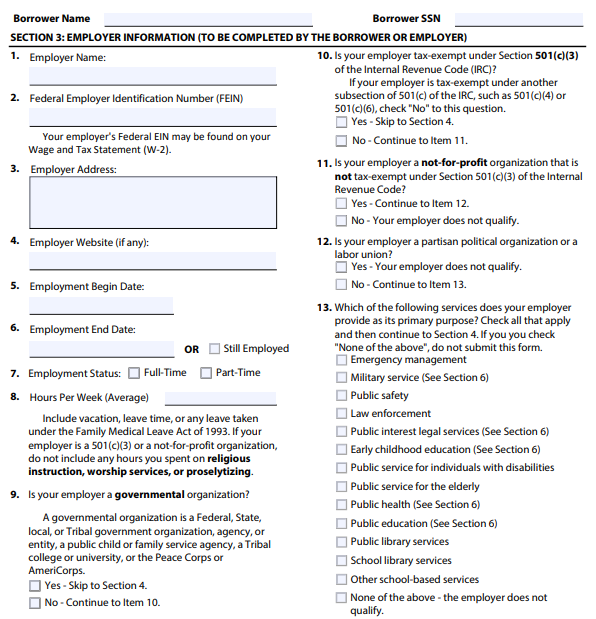

One of the most common and well-known programs for federal loans is called the Public Service Loan Forgiveness (PSLF).

To be eligible for PSLF, you must work for a qualifying employer and make 120 qualifying payments before your remaining loan balance will be discharged.

Qualifying employers include:

- Government organizations at any level (federal, state, local, or tribal)

- Tax-exempt, nonprofit organizations

- Other types of nonprofit organizations that are not tax-exempt if their primary purpose is a qualifying public service, like public health, and

- AmeriCorps or Peace Corps, if you’re serving as a full-time volunteer.

PSLF applies to borrowers who have been paying on an income-driven repayment plan for 10 years, and only Direct Loans are eligible.

Income-driven repayment plan forgiveness

Student loan forgiveness for specific jobs

Some professions offer student loan forgiveness either through a federal, state or local program.

One example is the Teacher Loan Forgiveness Program designed for teachers serving low-income communities. For this program, the following loans qualify:

- Federal Direct Loans (subsidized or unsubsidized)

- Federal Stafford Loans (subsidized or unsubsidized)

- Federal Direct Consolidation Loans

Here’s what you need to know about the terms of the program.

Doctors and other medical professionals also have several options for getting their loan balances discharged.

Closed-school loan discharge

If your school is no longer open, you may be able to have your loans forgiven. You can be get your Direct Loans, Federal Family Education Loans (FFEL) and federal Perkins Loans completely discharged by calling your loan servicer to start the process.

You are eligible for this if were not able to complete your program because your institution closed, and if

- You were enrolled when your school closed,

- You were on an approved leave of absence when your school closed. or

- Your school closed within 120 days after you withdrew.

Total and permanent disability student loan discharge

It a serious health issuecauses you to have trouble supporting yourself, your loans could be discharged based on the permanent illness or disability.

See also: The Best Student Loan Forgiveness Programs

It’s not an easy process, however. Going this route, you’ll be expected to demonstrate your need for loan forgiveness in one of the following three ways (which are explained in detail through a dedicated website):

- If you’re a veteran, you can submit documentation from the U.S. Department of Veterans Affairs showing that you have a service-connected disability that is 100% disabling.

- The Department of Education contacts you directly if it is notified by the Social Security Administration that you are receiving Social Security Disability Insurance or Supplemental Security Income benefits and you have a disability review within five to seven years from the date of your most recent SSA disability determination.

- You can submit a certification of your total or permanent disability from a U.S. licensed-doctor.

State programs

In addition to federal programs, many states have their own student loan forgiveness programs. See below to find out more about your state.

Eligibility

As there are different programs with different requirements that you allow you to discharge your loan balance, you need to know which one(s) you’re aiming for in order to determine eligibility. Most of the programs, however, require you to make a certain amount of payments, or make payments for a certain amount of time, before your loan balance can be forgiven.

Public Service Loan Forgiveness eligibility

For the most common, PSLF, you should be eligible if you work full-time for a qualifying employer, regardless of your specific job title. Generally, these types of employers qualify for PSLF:

- Federal, state, local, or tribal government organizations.

- 501(c)(3) nonprofit organizations.

- Non-501(c)(3) nonprofits that provide public services as their primary mission.

If you plan on applying for the PSLF, for instance, in addition to working for a qualifying employer, you must:

- Be enrolled in one of four income-driven repayment plans.

- Make 120 qualifying, on-time payments.

- Have a Direct Loan.

Income-driven repayment plan forgiveness eligibility

Borrowers who have made payments toward their loans on an income-driven repayment plan and have still not paid off their loan at the end of their repayment terms are eligible for forgiveness.

Student loan forgiveness for specific jobs

Each career-specific loan forgiveness program, like those for doctors, lawyers and teachers, will have its own set of requirements. As an example, Teacher Loan Forgiveness Program is for teachers who have a Federal Direct Loan, Federal Stafford Loan, or Federal Direct Consolidation Loan. Applicants must:

- work in a public or nonprofit school, and

- teach in a critical shortage area (such as math or science),

- work with students with disabilities or

- work in a school that serves low-income students.

Potential downsides to consider

There a few things to look for if you’re banking on student loan forgiveness … and the first one is a biggie.

PSLF is not guaranteed. A recent report by the Government Accountability Office shows that 99% of people who applied for PSLF the first year forgiveness was available were denied.

See also: Breaking: 99% of People Who Apply for Student Loan Forgiveness Get Denied

Loan forgiveness takes a long time. Remember, the longer you’re paying on a loan, the longer you’re paying interest on that loan. You have to consider whether it’s worth it to you to drag out your loan payments for 10, or even 20-25 years, depending on which forgiveness program you plan on using.

You may not actually save any money. By the time you’re finally able to zero-out your loan, you may be close to paying it off. Ask your loan servicer to run some numbers for you to see if waiting is worth it. It may actually be better to pay off your loan faster by paying ahead or refinancing. The faster you’re able to stop paying interest, the more money you’ll save.

See also: The 1 Thing You're Probably Not Doing That Could Save You Big Time on Your Student Loans

You may have to pay taxes on your forgiven loan balance. If you get loan forgiveness after 20-25 of using an income-driven repayment plan, you’ll have to pay taxes on the remaining balance. For example, if you have $10,000 in debt that is excused, that $10,000 will be treated as income on your tax return. So if you would’ve made $70,000 the year that your loans were forgiven, you would have to pay taxes on $80,000.

Loan balances forgiven through PSLF or through disability forgiveness do not come with a tax penalty.

Frequently Asked Questions (FAQs):

- How do I know if qualify?

- Can I get student loan forgiveness for my Navient, NelNet or Great Lakes loans?

- Can I have student loans forgiven if they are in default?

- How do I apply for student loan forgiveness?

- Where is the student loan forgiveness application?

- What should I do if my student loan forgiveness was denied?

- What student loan forgiveness scams should I avoid?

- What is Obama student loan forgiveness?

- Are there legitimate student loan companies that can help with loan forgiveness?

How do I know if I qualify?

Public Service Loan Forgiveness

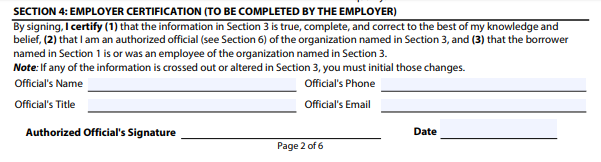

To make sure you’re eligible for PSLF, you’ll need to complete the Employment Certification for PSLF Form once a year and each time you change employers. This way, you’ll know that payments you make on your loan are counting toward your 120 qualifying payments. (Not taking this step is one of the several ways people mess up when it comes to PSLF.)

Remember, only Direct Loans qualify for PSLF. If you have other federal loans, they can become eligible for PSLF if you consolidate them into a Direct Consolidation Loan. If you want to go this route, make sure to consolidate as soon as possible. Any payments you make before you consolidate do not count toward your 120 qualifying payments.

In addition, you need to make sure your 120 payments are on-time. If you make a payment 15 days past the due date, it doesn’t count toward the 120.

Forgiveness after income-driven repayment

You should be eligible for forgiveness if you have reached the end of your repayment term under an income-driven repayment plan and you still have not fully paid off your loan. The repayment terms are:

- REPAYE Plan: 20 years for undergraduate studies, 25 years for graduate or professional studies

- PAYE Plan: 20 years

- IBR Plan: 20 years if borrowed on or after July 1, 2014, or 25 years if you borrowed before July 1, 2014

- ICR Plan: 25 years

Can I get student loan forgiveness for my Navient, NelNet or Great Lakes loans?

Navient, NelNet and Great Lakes are servicers of federal student loans. That means that your payments to these servicers may count toward your payment obligations for PSLF or for forgiveness through income-driven repayment.

However, you need to make sure that the loans you have with these providers are the exact loans that qualify under the specific forgiveness program, and that you otherwise qualify for forgiveness. For example, for PSLF, only Direct Loans qualify.

If your current loans don’t qualify, you can consolidate them into a Direct Loan in order to be eligible for PSLF and other loan forgiveness programs under which Direct Loans qualify. But only payments made after consolidation will count toward your payment obligations for forgiveness.

The good news is that, as loan servicers, Navient, NelNet, and Great Lakes can help you get on the right path toward loan forgiveness. Be sure to call your servicer to find out which type of loan you have before relying on loan forgiveness.

Can I have student loans forgiven if they are in default?

No, you must be current on your loans to qualify for PSLF. Remember that you must make 120 qualifying, on-time payments before your loan balance can be forgiven. If you need help getting your loans in good standing, call your loan servicer and ask for help. Be sure to tell them you plan to apply for PSLF so that they put you on the right path.

How do I apply for student loan forgiveness?

Public Service Loan Forgiveness

Each loan forgiveness program has a different application processes, so you’ll need to check individual programs for more information.

For the PSLF, you must submit an application and still be working for a qualifying employer at the time you complete your 120th payment. Your loans won’t be forgiven automatically when this last payment is made, however. You must fill out the application to begin the process.

See also: How to Apply for Public Service Loan Forgiveness

Forgiveness after income-driven repayment

Your loan servicer will notify you if and when you close to of qualifying, but you may also contact your loan servicer if you believe you qualify and you have not been contacted yet.

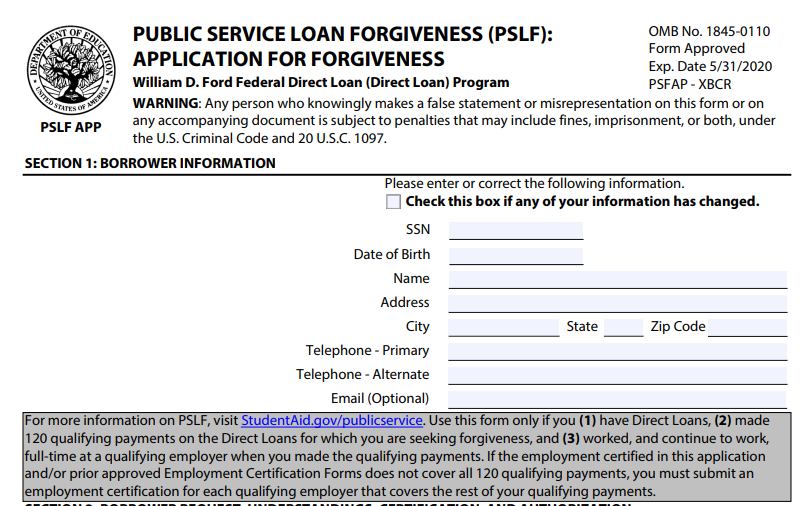

Where is the student loan forgiveness application?

The application for PSLF, shown below, can be found on the federal student aid website.

Following the instructions on the application, you’ll be well on your way to getting your loan balance discharged. As a reminder, your employer will need to certify your employment on this form, too.

See also: How to Apply for Public Service Loan Forgiveness in 5 Steps

What should I do if my student loan forgiveness was denied?

If you went through the 10-year process for PSLF, and you were denied, know you’re not alone. This is a common issue borrowers have encountered.

The good news: You have a second chance under a Congress-approved fix called the Temporary Expanded Public Service Loan Forgiveness (TEPSLF). This loosens the rules a little bit to bring relief to borrowers who bargained on getting their loan balance discharged but were denied PSLF.

Here’s what you need to know. This temporary fix applies to you if you were rejected for PSLF and you:

- Were enrolled in an extended or graduated repayment plan, rather than an income-driven repayment plan. (You don’t have to switch to income-driven plan to qualify now.)

- Have Federal Direct loans.

- Paid as much in the past 12 months as would have under income-driven repayment.

To apply for TEPSLF, send an email to FedLoan Servicing at TEPSLF@myfedloan.org.

See also: Breaking: You Just Got a Second Chance at Student Loan Forgiveness

What student loan forgiveness scams should I avoid?

Student loan financing can seem ripe for scams. Since borrowers are hungry for relief from student loan debt, they’re often willing to try anything, and some companies promise to offer help — sometimes for a fee.

This may be a scam. When it comes to student loans, your lender or loan servicer can help you for free.

See also:

What is Obama student loan forgiveness?

In the case of student loan forgiveness, a company that promises to reduce or eliminate your debt is likely a scam. Federal student loan forgiveness programs are available for public servants, teachers, medical professionals, and even for residents in specific states and other professions.

One such scam is companies who refer to the “Obama student loan forgiveness” program.

There is no such program. These companies charge fees to enroll in the same federal student loan forgiveness programs that are available to everyone for free.

Your approval for federal student loan forgiveness programs is not contingent on help from a private company. You just have to meet the eligibility requirements.

Are there legitimate student loan companies that can help with loan forgiveness?

If you believe you meet the requirements for PSLF or another loan forgiveness program, you can work directly with your loan servicer. Your loan servicer will certify you as eligible for loan forgiveness to ensure that you qualify before you go through the entire process.

In other words, legitimate servicers of federal loans can help you with the process for free.